The cash conversion cycle (CCC) measures the number of days it takes to convert inventory investments into cash. While the premise may sound complicated, it’s easy to calculate these cash conversions if you understand the formula.

Overview: What is the cash conversion cycle?

There are a lot of financial ratios small business owners can calculate to get a good handle on business performance. While you’re probably familiar with commonly used ratios such as the debt-to-equity ratio, the current ratio, or the quick ratio, the CCC may not be on your radar.

Sometimes referred to as the cash cycle, or the net operating cycle, the CCC is important, particularly if you purchase and move inventory regularly.

That’s because the CCC provides you with a ton of information from a single calculation — such as how long it takes your business to convert its current inventory into cash or sales, how long it takes to collect on accounts receivable balances from customers, and finally, how quickly you need to pay your vendors and suppliers.

If you’re using accounting software, you can pull the totals you need to calculate your CCC directly from your financial statements.

How to calculate the cash conversion cycle

The formula for calculating the CCC is a multi-step process, requiring you to first obtain the following totals:

• Days of inventory outstanding, or DIO

• Days sales outstanding, or DSO

• Days payable outstanding, or DPO

Each one of these totals requires a separate calculation, with the results of those calculations the basis for calculating the CCC.

You’ll also need to have the number of days in the period for which you’re calculating the CCC. For example, if you’re calculating it for the entire year, you would use 365 days.

If you’re calculating for a month or a quarter, you would just use the number of days in that particular time frame. Once you have all of this information, you can calculate the CCC using the cash conversion cycle formula:

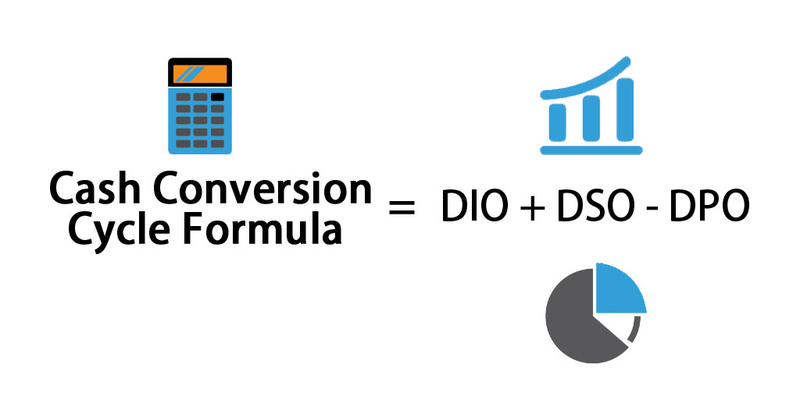

DIO + DSO – DPO = CCC

An example of the cash conversion cycle

Sam manufactures and sells custom cabinets. To get a better handle on his business, Sam decides to calculate the CCC for his business for 2019. There are numerous steps Sam needs to take.

Step 1: Calculate DIO

Sam first needs to calculate his days of inventory outstanding, or DIO. This is used to determine the number of days it takes to turn inventory into sales, with DIO indicating the number of days inventory is held before it’s sold.

To calculate DIO, Sam will need to obtain his beginning and ending inventory totals for 2019. He’ll also need to obtain the cost of goods sold for that same period.

On Sam’s income statement, his beginning inventory for 2019 was $9,800, and his ending inventory balance was $8,200, with the cost of goods sold for the year totaling $98,000. He can now calculate his DIO:

($9,800 + $8,200) ÷ 2 x 365 = 33.52

$98,000

This means that it takes Sam approximately 34 days to turn his inventory into sales.

Step 2: Calculate DSO

The second step is to calculate days sales outstanding, or DSO. An important metric on its own, DSO indicates the number of days it takes to collect on accounts receivable balances after a sale has been made.

To calculate DSO, Sam will need to obtain his average accounts receivable balance for the period, along with his total credit sales for the year.

Sam’s beginning accounts receivable balance in 2019 was $14,000, with an ending accounts receivable balance of $10,000, with both of these totals available on his balance sheet. Next, Sam needs to get his total credit sales for the year from his income statement, which is $205,000.

With these totals in place, Sam can complete the DSO calculation:

($14,000 + $10,000) ÷ 2 X 365 = 21.36

$205,000

This result indicates that it’s taking Sam 21 days on average to collect payment on an invoice.

Step 3: Calculate DPO

The third step is to calculate the number of days that it takes a business to pay its creditors, vendors, and suppliers, or days payable outstanding. To calculate DPO, Sam will need to obtain his beginning and ending payables balance from his balance sheet, as well as the cost of goods sold for the period.

Sam had a beginning accounts payable balance of $7,500 and an ending accounts payable balance of $8,100. His cost of goods sold for the year was $98,000, the same amount that was used to calculate days inventory outstanding. Sam can calculate the days payable outstanding as follows:

($7,500 + $8,100) ÷ 2 x 365 = 29.05

$98,000

This result indicates that it takes Sam’s company 29 days on average to pay its bills.

Step 4: Calculate CCC

The final step is calculating the CCC. This is done by adding together the DIO and DSO and subtracting the DPO.

33.52 + 21.36 – 29.05 = 25.83

Sam’s CCC is 25.83, meaning that it takes Sam’s company approximately 26 days to turn its inventory into cash.

Cash conversion cycle frequently asked questions

What is a good CCC?

The lower the CCC your business has, the better. A negative number is best since that means you maintain limited inventory, get paid quickly, and typically don’t pay creditors until after your customer pays you.

Why should I calculate the CCC for my business?

While the CCC is useful for creditors and potential investors, knowing the cash conversion cycle is helpful for you as well.

For instance, calculating the CCC can show how efficient your business is operating, whether you’re collecting payments from your customers on a timely basis, and even how well your products are selling.

If I don’t have inventory, is the CCC still useful?

Other accounting ratios are more useful for businesses without inventory, such as the current ratio, quick ratio, liquidity analysis, or accounts receivable turnover ratio, all of which are better suited to businesses without inventory.

A final word about the cash conversion cycle

Also known as the net operating cycle or cash cycle, the cash conversion cycle measures business performance step by step from initial inventory purchase to how quickly your business pays vendors and suppliers for purchases.

The CCC can tell you a lot about your business, but it requires multiple steps and calculations before the final figure is reached. The ideal CCC number will be on the low side, which indicates that your business can sell inventory and collect on those sales quickly.

Knowing your CCC can provide you with the information you need to make needed adjustments in your business, from increasing sales to collecting on those sales invoices.

If your small business does not have inventory on hand, there are other calculations more suitable, but if your business involves selling inventory, calculating the CCC is always a good idea.

The post The Cash Conversion Cycle and How to Calculate It for Your Business appeared first on The blueprint and is written by Mary Girsch-Bock

Original source: The blueprint