As an accountant, one of the skills I appreciate the most in small business owners is records management. Business owners are told to keep track of tons of records — schedules and forms, even the ones you accidentally spilled maple syrup on — and I’m here to tell you about one more: depreciation schedules.

The next time your business makes a large asset purchase, follow this guide to create your depreciation schedule.

Overview: What is a depreciation schedule?

Depreciation schedules serve as a roadmap to an asset’s depreciation expenses. Businesses create depreciation schedules to outline how a fixed asset’s costs are expensed over its useful life.

You can’t immediately write off the purchase of many fixed assets. Instead, you expense the cost over its useful life, which is the expected amount of time the asset will generate revenue and be of use to your business.

Generally Accepted Accounting Principles (GAAP) allow you to choose one of four depreciation methods. The IRS offers less flexibility, requiring that you follow its proprietary depreciation method for most assets.

What kind of assets do you depreciate?

Fixed assets that won’t be consumed within one year are subject to depreciation. Your building, factory equipment, computer, and furniture are considered fixed assets and may be depreciated.

Intangible assets, such as email lists or patents you bought from a third party, are subject to amortization, which is the word used for the depreciation of intangible assets.

The grand exception to depreciation is land. You don’t depreciate land because it has an unlimited useful life. Greta Thunberg might disagree with that, but she can take it up with the Financial Accounting Standards Board (FASB).

You don’t depreciate all assets. Office supplies, inventory, and low-cost items don’t get the same treatment because they usually get used up in a year or less.

Methods of depreciation

As a business owner, you get to pick among four depreciation methods for financial reporting. While you can use different depreciation methods for different asset classes, most small businesses should stick to just one.

Every asset gets its own depreciation schedule, so you must calculate depreciation for every depreciable asset.

1. Straight line

Most businesses use the straight line method for depreciating assets. Most of the time there’s no good reason for a small business to choose any other method.

Under the straight line method, your business asset is depreciated by a uniform amount for every year of its useful life. You divide each asset’s depreciable value (cost – salvage value, or the value at the end of the asset’s useful life) by its useful life to get the annual depreciation expense.

2. Double declining balance

The double declining balance method front-loads your depreciation expense. As the asset ages, annual depreciation expense declines.

This accelerated depreciation method can match the actual value of assets that lose value quickly at the beginning of their useful lives, like vehicles.

You calculate double declining depreciation by doubling the straight line depreciation rate. For example, say an asset’s depreciable value is $10,000, and it has a useful life of five years. The annual straight line depreciation would be $2,000 ($10,000 / 5 years).

The straight line rate is 20% ($2,000 annual depreciation / $10,000 depreciable value), meaning the double declining rate is 40%.

For subsequent years, apply the 40% depreciation rate to the remaining net book value (book value – depreciation).

3. Sum-of-the-years’-digits

Businesses might use the sum-of-the-years’-digits method when their assets tend to lose the most value at the beginning of their useful lives.

Start the sum-of-the-years’-digits calculation by summing the years of the asset’s useful life. If your asset has a five-year useful life, the calculation is:

1 + 2 + 3 + 4 + 5 = 15

For the first year, divide the asset’s useful life — in this case, 5 — by the sum of 15. Multiply that number by the asset’s depreciable value. If the asset’s depreciable value is $10,000, the first year’s depreciation is $3,333 [(5/15) x 10,000].

Most of the formula stays the same in subsequent years; just reduce the numerator by one every year.

4. Units of production

Manufacturing businesses often use the units of production method for their machinery. Instead of having a useful life measured in years, you determine the number of units a machine can produce in its useful life.

Say a machine has a $10,000 depreciable value and can produce 100,000 units in its useful life. For every unit the machine produces, you charge 10 cents to depreciation expense.

5. Modified accelerated cost recovery system

You must use the methods above on your financial statements, but the IRS requires that you use its proprietary depreciation method on your taxes for most assets. It’s called the modified accelerated cost recovery system (MACRS, pronounced “makers”).

Depreciation causes permanent differences between your book and taxable income due to the use of different depreciation methods. Trust your tax software or a tax professional to help you complete a tax depreciation schedule.

MACRS usually follows the straight line or double declining method. IRS Publication 946 determines each asset’s useful life and explains all the depreciation and amortization rules and regulations.

Sole proprietorships and single-member LLCs deduct depreciation when they fill out Schedule C on Form 1040.

How to set up an asset’s depreciation schedule

Each asset should have its own depreciation schedule, which you can aggregate onto another schedule that gives you a glance at all your depreciable assets.

You should make your depreciation schedule in a spreadsheet. You can find endless template options on the Microsoft website. I made my own because, as Tabitha Brown says, that’s my business.

Let’s create a business vehicle depreciation schedule. At the top of your depreciation schedule, list the following information:

• Asset name

• Purchase date

• Purchase cost

• Salvage value

• Depreciable value (purchase cost – salvage value)

• Useful life

• Depreciable method

The most important part of the depreciation schedule is a table that lists annual depreciation for the asset. The table should include:

• Starting asset net value

• Cumulative depreciation, which is the total amount depreciated on the asset

• Annual depreciation expense

• Ending asset net value

You’ll know you’ve created an accurate depreciation schedule when your net book value at the end of the asset’s useful life equals your asset’s salvage value.

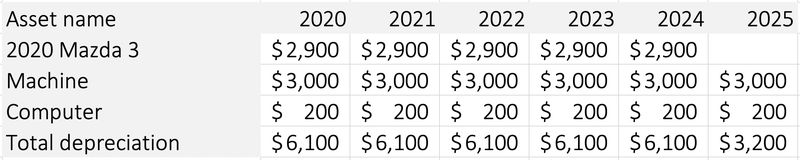

How to build a total fixed asset depreciation schedule

Once you make the asset’s depreciation schedule, add it to your list of depreciable assets. The goal of a total fixed asset depreciation schedule is to help you book your depreciation journal entry.

Your depreciation expense balance on your income statement should equal the “total depreciation” row on your fixed asset depreciation schedule.

Depreciation schedule frequently asked questions

Can I make changes to my depreciation schedules?

You should only adjust your depreciation schedule when you notice a clerical error. In most cases, you can correct the mistake by recalculating depreciation going forward.

Fixed assets that break, become obsolete, or otherwise permanently lose their value might need to be impaired. An accountant should regularly test your fixed assets for impairment and help you adjust your depreciation schedules accordingly.

Consult a CPA when you catch a mistake or think your asset might be impaired. Some changes might require you to amend your business tax return or restate your financials.

Can I use MACRS for financial reporting?

MACRS, the depreciation method for business taxes, usually requires shorter useful lives than you would deem appropriate, and it doesn’t allow for salvage value. Don’t use MACRS for financial reporting purposes.

GAAP requires that you use one of the following methods:

• Straight line

• Double declining balance

• Sum-of-the-years’-digits

• Units of production

How do I calculate an asset’s depreciable value?

The two components of an asset’s depreciable value are its purchase price and salvage value. The purchase price includes tax, shipping, warranty, and insurance costs. Maintenance fees aren’t included in your depreciation calculation.

The salvage value is the expected value of the asset at the end of its useful life. Businesses often assess salvage value at $0, meaning it’s worthless at the end of its useful life.

Schedule your depreciation on day one

Set up an asset’s depreciation schedule right away. When you file your small business taxes and create your annual financial statements, you want to have your depreciation schedules ready to go.

The post How to Make a Depreciation Schedule: A Small Business Guide appeared first on The blueprint and is written by Ryan Lasker

Original source: The blueprint