It’s practically a universal truth: having a low credit score is bad. But what you may not realize is that having a low credit score can have an effect on more than just your finances. It can have far-reaching consequences, including limiting the kind of lifestyle you’re able to attain and even weighing on your mental health.

Those with a credit score within the 300 to 549 range report their poor credit history has impacted their housing, careers, relationships and even their ability to communicate. In fact, about 28% of those with poor credit say they can’t rent the apartment they want, while 22% have been denied a cellphone plan, according to a new survey from Credit Sesame of 5,000 U.S. adults.

About 14% of Credit Sesame respondents have what’s considered to be a poor credit score under 549. Roughly 17% had a fair score of 550 to 639, while 20% had a good score (ranging from 640 to 719) and 41% had excellent credit (720 to 850). FICO scores range from 300 to 850.

Among Credit Sesame’s survey, respondents with poor credit tended to be young, female and don’t have a college education.

“I have trouble paying bills because daily living is so expensive, and I am already working all the time,” one respondent said.

“It’s expensive to have poor credit,” says Jay Moon, general manager of Credit Sesame’s credit business. Improving your credit score by just 35 points — from roughly a sub-prime score of 660 to a good score of 695 — can save you $301 a year in interest charges, according to an analysis by bill pay service doxo.

But while a bad credit score can add more expenses in the form of higher interest rates and other fees, Moon says the cost of poor credit is “much bigger than just the direct financial costs.”

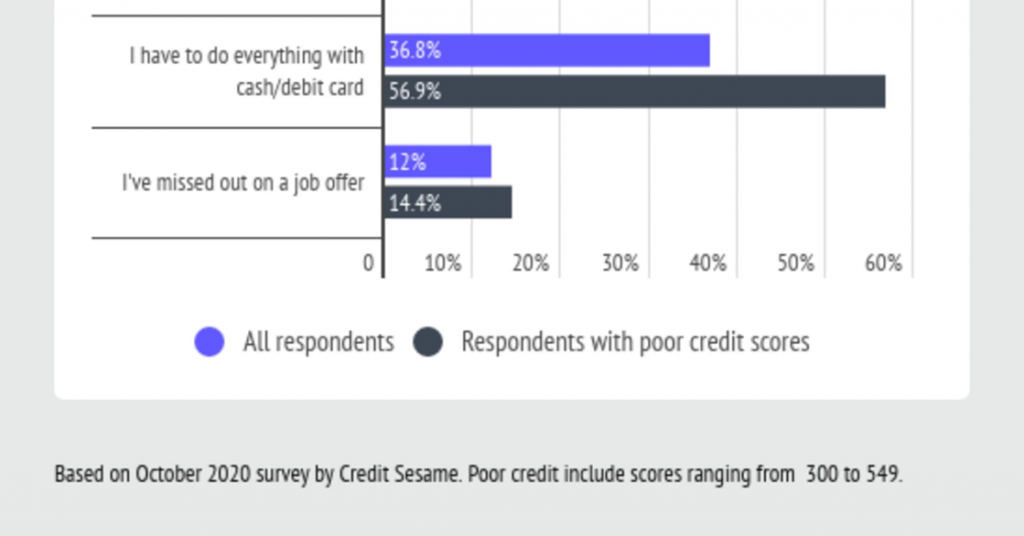

There are also long-term consequences: about 14% of survey respondents with low credit scores say they’ve missed out on at least one job opportunity because of their poor credit. And 10% say their low credit score has caused problems in their romantic relationships.

About half of those with scores between 300 and 549 can’t buy a home or qualify for a car loan. And 57% say they have to use cash or debit cards because they can’t get approved for a credit card.

The emotional and mental toll that having a bad credit score should not be overlooked. About 79% of those surveyed with low credit scores say the situation induces negative feelings, with worried (49%), ashamed (46%) and angry (30%) being the most common. Over half, 58%, believe that there aren’t fair credit options for them and about 43% actually report having a credit score hurts them a lot.

That’s a stark contrast to those who have good (scores between 640 and 719) or excellent (720+) credit, commonly reporting their scores make them feel proud, happy and fine. Additionally, 2 out of 3 of these respondents felt their scores were a fair and accurate reflection of their creditworthiness.

How to improve your credit situation

For those struggling with bad credit, Moon says there are steps you can take to do something about it. “You’re not just going to have to stay in a poor credit situation,” he says.

Instead, he recommends the first step is to boost your knowledge about how credit scores work. Services like Credit Sesame and Credit Karma, but also many credit card companies, allow you to access and track your credit score for free so you can learn how spending habits can affect your score.

Not only should you educate yourself on your personal score and spending, but Moon says it’s also important to pay attention to what’s happening in the industry as well. Earlier this year, for example, Congress and private lenders rolled out a number of forbearance and payment deferral programs aimed at helping those financially affected by the Covid-19 pandemic. If you’re struggling right now, Moon recommends taking advantage of these programs to make sure you can maintain a good and healthy credit score.

Additionally, Moon recommends that those with lower scores pay attention to some of the innovations coming down the pipeline that could provide a much fuller picture of credit worthiness. Experian Boost, for example, allows consumers to link their monthly utility and telecom bills to get credit for on-time, complete payments.

A good way to approach your credit score is by thinking about it as being “fundamental” to your overall financial health and wellness, Moon says. Just as you would exercise and eat right to maintain your physical health, Moon says consumers need to take the proper steps to keep their credit score in check or even boost it.

The post A poor credit score affects more than just getting a loan or credit card appeared first on CNBC News and is written by Megan Leonhardt

Original source: CNBC News